The world is in full lockdown and so am I. Taking the virus extremely serious and protecting those vulnerable around me, I am limiting my interactions with others as much as possible. I am staying at home and cancelled all planned trips for the coming months.

This being said, It’s been a very interesting few weeks. Working from home (instead of from coffee shops), exercising at home (instead of at the gym), cooking all meals (instead of eating out), exploring nearby hiking trails and going camping in the wilderness (instead of traveling to foreign countries and new places).

Note: Given what the world is currently going through, I don’t feel like writing an extensive update about the perks of passive income and financial independence. This is not a “happy” or “positive” update. It’s just an update for the record.

May 2020 Passive Income Investment Portfolio

May 2020 Passive Income Update

My total passive income in April 2019: – P2P lending: 395.88EUR – Real Estate Lending: 49.59 EUR – ETF Dividends: 64.56 EUR – Stock Photos/Videos: 115.25 EUR TOTAL: 625.29 EUR (~693.73 USD)

P2P Lending & Real Estate Lending Update – May 2020

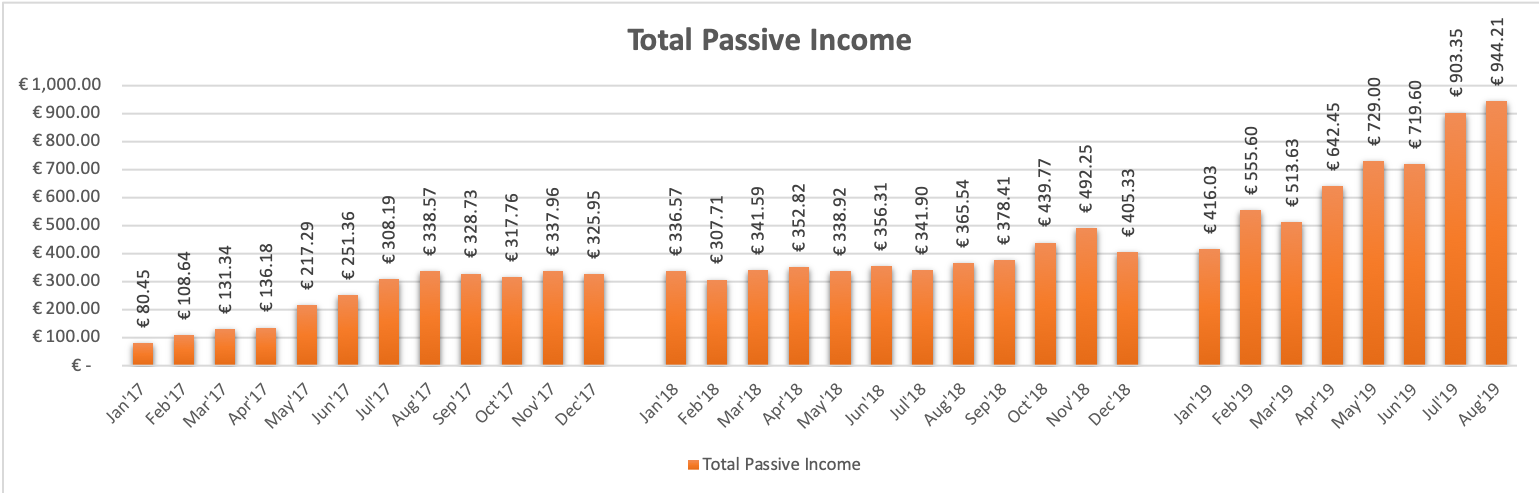

Total Passive Income from P2P Lending, P2P Real Estate Lending, ETF Dividends and Stock Sales.

My favorite park for social distancing running/walking here in Phoenix/Arizona.

P2P & Real Estate Lending Overview – May 2020 Passive Income Update

As part of my May 2020 passive income update, here is a quick overview of passive income that I was earning this past month from three (3) P2P Lending and two (2) Real-Estate P2P Lending platforms that I am currently investing in.

Given the uncertainty around the short- and long-term economic ramifications of COVID-19, I believe that there is a real chance that lenders will struggle to pay back their loans, which in turn could lead to delayed payments, P2P lending platforms and loan orgiinators struggling with payback guarantees, etc. For that reason, I am reminding myself that I should only invest what I can afford to lose. P2P lending is a form of high-risk investment which remains to large extend unregulated.

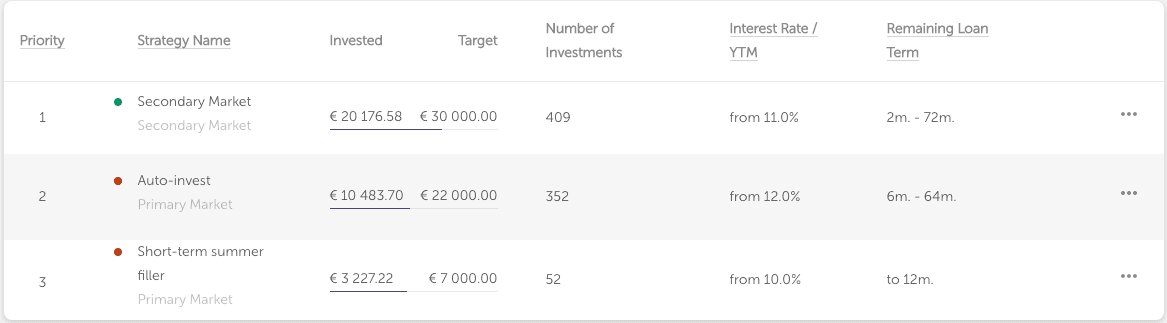

Mintos: With 32,100 EUR auto-invested on Mintos in loans from 24 loan originators (all with ratings from A+ to B) in 20 countries, my interest income from Mintos in April was 259.91 EUR (=self-calculated interest rate of 7.90% p.a.).

I noticed that some investors started panic selling some of their loans with a steep discount (see graphic below) of up to 14.5% discount on the secondary market. Either they need the money to survive the coming months or they are scared to lose it. I adjusted by auto-invest portfolios to only buy loans on the secondary market that are sold with a discount.

Mintos Auto-invest portfolios (May 2020). Only buying loans from the secondary market at a discount.

Swaper:I had decided to pause my auto-invest portfolio at the beginning of March. I have since received interest and principal payments from my ongoing loans, the majority of which were on-time.

I withdrew incoming interest and principal payments in batches over the past weeks and have so far “cashed out” 5,100 EUR out of my 9,000 EUR total invested. The remaining 4,900 EUR are unfortunately loans that are delayed or extended. What is working great is Swaper’s buyback, which has kicked in and buys back loans from me that are more than 30 days late.

Another positive aspect: Every time I made a withdrawal transfer from my Swaper account, the money arrived in my bank accountwithin 48 hours.

Due to me pausing my auto-invest and withdrawing funds, my passive income frin Swaper in April was only 81,65 EUR (= 8.74% p.a.). As I am not re-investing, my average interest rate is lower than the 14/16% interest that I received on individual loans.

It will be interesting to see what the loan performance of Swaper will be over the coming weeks given the COVID-19 pandemic. Considering that Swaper specializes in short-term loans (14 and 30-day loans), their business might pick up given that Government aid arrives delayed in many COVID-19 affected countries.

My Swaper monthly income and interest rates

Grupeer: Grupeer is facing allegations from investors about fake loan originators on the Grupeer platform. Grupeer notified investors on March 31 that all payments to investors of Grupeer are currently suspended, with the official reasons stated being the state of emergency declared in the European Union and worldwide regarding the COVID-19 pandemic outbreak.

A number of investors are preparing legal action against Grupeer. Any Grupeer investor is able to join the legal action/law suit. More info here: https://sites.google.com/view/grupeerarmada/

I have 12,600 EUR invested on Grupeer and am emotionally preparing myself that either some or all my investments on Grupeer might be lost. I will update my blog with any information or updates that I receive.

Twino: A good month! My total investments of 7.500 EUR on Twino are fully invested. My April income from Twino was 54,32 EUR in interest payments (= 8.56% interest p.a.).

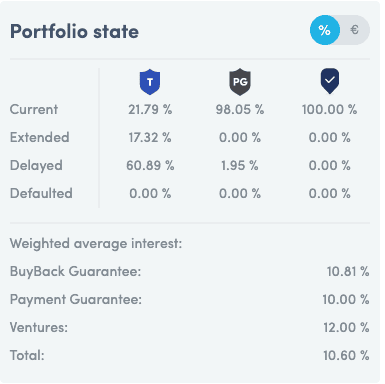

I decide to keep my auto-invest running on Twino for the time being. As of today, 60% of my loans with BuyBack guarantee are delayed – and I will keep an eye as to whether timely BuyBack guarantee is honored.

If you wonder, why you have never heard of Twino. The platform does not pay any referral credit to bloggers for which reasons many bloggers do not talk about the platform.

Twino Portfolio Stats May 2020 – 60.89% of loans with BuyBack Guarantee delayed. Not ideal!

EstateGuru: A good month on EstateGuru. After I increased my investments on EstateGuru to 5.000 EUR in December 2019, I am fully invested in 16 real estate projects in Estonia, Latvia, Finland and Lithuania.

15/16 projects are performing on time and 1 project is 16-30 days late. My average interest rate on EstateGuru is 10.82% p.a. For me EstateGuru is a great platform to diversify my risk by investing in real estate loans that are either secured with a first-rank mortgage (physical security), personal guarantees, or are backed with a mortgage.

As I mentioned in previous posts, almost all my loans on EstateGuru are either bullet or full bullet loans, which means that either principals or both interest+principals are being paid in full at the end of the loan period. Unfortunately, that means that some months I receive large interest and principal payments, some months I receive nothing. In April, I received 49.59 EUR in interest payments.

What else? My EstateGuru review explains details as well as shows how to receive a 0.5% bonus as a new investor in the first three months. I just saw that EstateGuru has some new loans available (10.5% p.a. & 12.00% p.a.).

My EstateGuru portfolio as of 1 May 2020 (c) EstateGuru

CrowdEstate:As I have mentioned in previous posts, my experience on CrowdEstate is negative and I am on my way out. 3 out of 6 projects are significantly delayed (90+ days) and bankruptcy has been filed against one borrower (H.M Seafood OÜ) for non-payment of debts and the refinancing planned by the sponsor to repay another of my loans failed (Kreutzwaldi 59c, 65610 Võru (IX)).

I suspended my auto-invest on CrowdEstate in January and withdrew my first 600 EUR in early February and another 450 EUR in March. The transfer arrived the next day, which was great. After my withdrawal, I still have a total of 950 EUR invested in CrowdEstate, which I will slowly withdraw as princial and interest payments are arriving. I decided to not offer my remaining loans on the secondary market (2% sell fee).

A photo from one of my many social distancing hikes over recent weeks.

Exchange–Traded Funds (ETF) Update – April 2020 🥳

Even in times of unstable (stock) markets, I hold onto my opinion that investing in the MSCI World ETF back in 2016 was one of the best decisions of my life. I am explaining details in my ETF portfolio post, but in a nutshell, I believe there is no better and more cost-effective way to save & invest long term (e.g. for retirement) while earning passive income from dividends.

Since I started investing in the MSCI World ETF in 2016, the value of the ETF has increased by 37.75% (despite the recent coronavirus-related shock in stock markets). The shares that I bought originally for 145.09 EUR a currently valued 189.89 EUR.

Coronavirus and my ETF portfolio

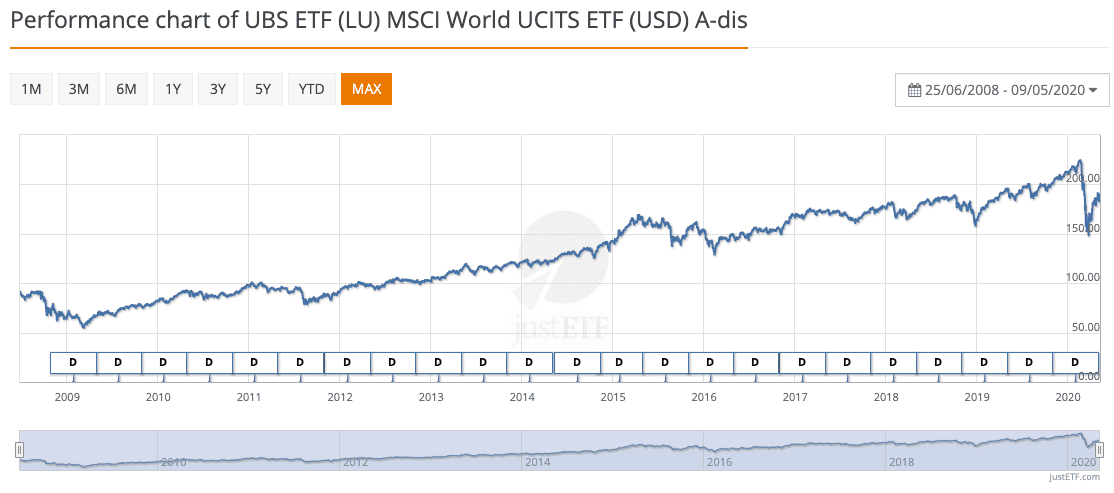

The spread of the Coronavirus (COVID-19) is severely affecting global economies and the 1600+ companies under the MSCI World are affected just as much. The UBS MSCI World that I have invested in since 2016 had temporarily dropped in value from 224 EUR to 164 EUR per ETF, but is now already back up at 189 EUR. In total numbers, that means that my ETF portfolio (~73,000 EUR) has lost 7,52% of its value this year, but is already on its path to recovery. I am not worried!

My ETF Portfolio since beginning of this year (c) justetf.com

Looking back at the past weeks, I wish I had bought more than 10,000 EUR given that the ETF is now back up to almost 190 EUR per share. Seeing the plummeting value of the MSCI World ETF in March, I bought an additional 10,000 EUR worth of UBS ETF (LU) MSCI World UCITS ETF (USD) A-dis shares (First 5k EUR tranche at 172 EUR/share and second 5k EUR tranche at 160EUR/share). I should have bought more.

Performance chart of MSCI World UCITS ETF (c) justetf.com

My 1,000 EUR monthly ETF savings plan

Many of you will know about my 1,000 EUR monthly ETF savings plan which I talked about in my January Blog Post. It’s automated, runs in the background, and keeps buying MSCI World ETFs worth 1,000 EUR on the first of every month. It’s a fantastic way of cost-averaging and keeps me committed to my financial savings goals. More about my ETF savings plan and why it was such a great idea to go back to an automated saving plan in this blog post.

That’s it for my May 2020 Passive Income Update! If you are interested, please follow my journey on my Facebook page Financial Freedom Journey for more frequent updates. And as always: If you have any questions or comments, please pop them in the comment section below. Or get in touch via Facebook or Email.

Stay safe, stay healthy, and please do practice social distancing, Peter 👋