Welcome to my February 2020 Passive Income Update.

January was a good month and the year started off really well. I returned to Istanbul, started Turkish classes, and enjoyed the mild winter weather in one of the most beautiful cities that I have ever lived in. ☀️

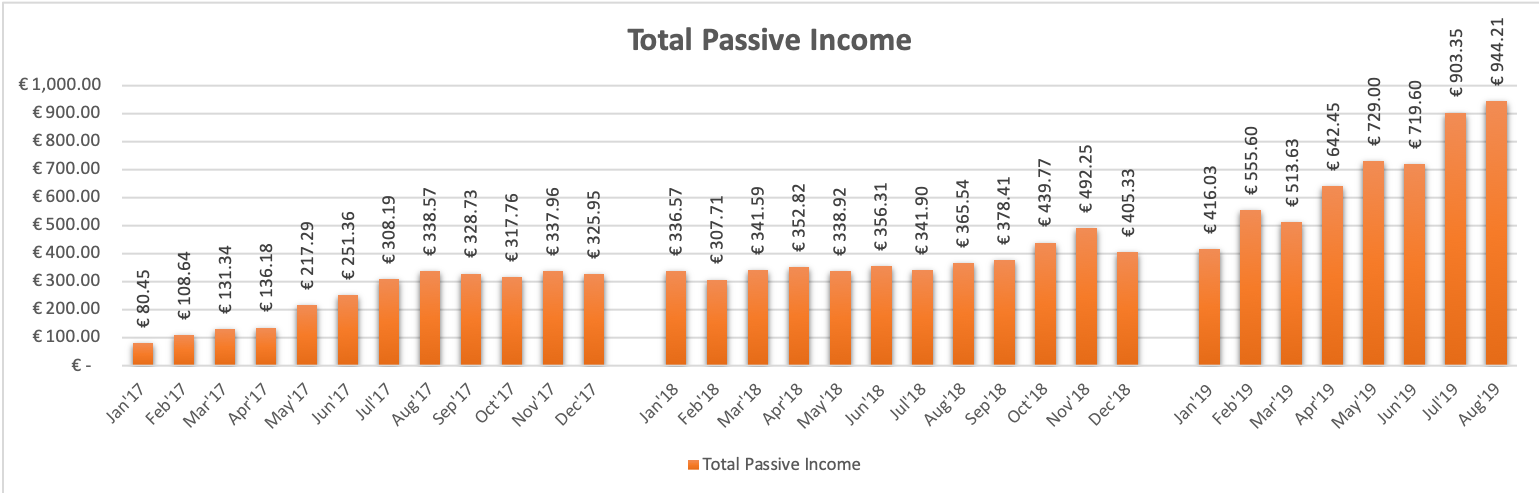

My passive income in January totaled 860.57 EUR (~954.74 USD) which is great! As 2020 unfolds, interest rates and loans availability are back to normal. More below.

January was a rocky month for the P2P market. While the European P2P market has many large professionally run platforms that offer good returns for reasonable risk (e.g. Mintos), the rapid growth and success of the market have led to a large number of small platforms popping up left and right.

Many of the ‘new’ platforms have been attracting investors with extremely high promised returns (15-20 % p.a.) often from unclear investment opportunities. I personally am not trusting any of the new platforms, and luckily had not invested in either Kuetztal or Envestio which are two platforms that went sour this past month.

It is unclear but both platforms might have been a complete SCAM or might have been involved in fraudulent activities. Almost overnight both platforms vanished, with their websites disappeared. And investors with their investments left out in the cold. The police are now involved.

However, what is positive about the recent shakeup is that it gives the P2P lending market an important wake-up call. A call to be more cautious. A call to think twice and due a reasonable amount of research and due diligence before investing in a new platform. And a call to accept a certain residual risk when investing in P2P lending. Diversification is important, but that does not mean to invest in as many platforms as possible. Quality over quantity is my motto.

Now, on to my passive income numbers for this past month!

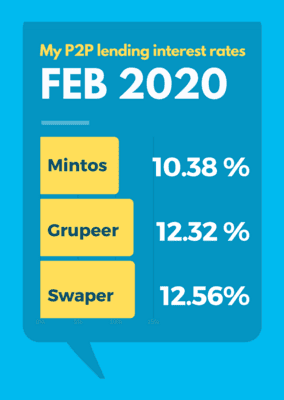

February 2020 P2P-Lending Interest Rates

February 2020 Passive Income Update

My total passive income in January 2019: – P2P lending: 617.89 EUR – Real Estate Lending: 75.33 EUR – ETF Dividends: 96.15 EUR – Stock Photos/Videos: 71.20 EUR TOTAL: 860,57 EUR (~954.74 USD)

P2P Lending & Real Estate Lending Update – February 2020

Total Passive Income from P2P Lending, P2P Real Estate Lending, ETF Dividends and Stock Sales.

P2P & Real Estate Lending Overview – February 2020 Passive Income Update

As part of my February 2020 passive income update, here is a quick overview of passive income that I am earning from four (4) P2P Lending and two (2) Real-Estate P2P Lending platforms that I am investing in.

Mintos: Loans with 10-11% are back. With next to no cash drag and incredible diversification possibilities, Mintos is and remains my absolute favorite P2P lending platform. No wonder, Mintos is by far the biggest P2P marketplace in the European P2P Lending market and allows for great diversification within the platform itself.

I have a total of 32,100 EUR invested on Mintos which represents 26% of my total investment portfolio. The money is spread across 24 loan originators (all with ratings from A+ to B) in 20 countries, which gives me a good diversification. My interest income from Mintos in January was 331.54 EUR with a self-calculated interest rate of 10.38% p.a.

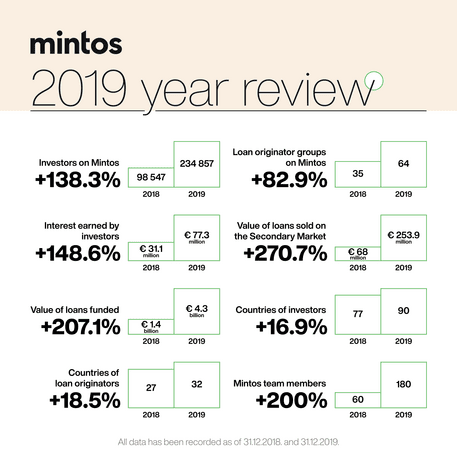

Mintos released its 2019 Numbers (see below), which are absolutely mindblowing. The value of loans funded through Mintos more than tripled to 4.3 billion Euro (3x increase). Today more than 234.000 investors are investing through the Mintos platform (2.3x increase). A team of 180 staff members are supporting the operations (3x increase).

Following the release of the numbers, I decided to increase my investments on Mintos this year. More soon.

My Mintos auto-invest portfolio is still including loans with interest rates starting from 9.0% (only accepting loan originators with A+, A, A-, B+, and B rankings and with BuyBack guarantee). If you are new to Mintos, have a look at my Mintos review which includes my auto-invest settings.

Mintos 2019 Performance. The Mintos team tripled within one year to 180 staff. Investors more than doubled to 234.000 investors, earning an average of 329 Eur per year. (C) Mintos

Swaper:After I lowered my investment on Swaper from 14,000 to 9,000 EUR in December due to heavy cash-drag, things have significantly improved. Over the past 4 weeks, I was almost fully invested with sometimes only 400-500 EUR awaiting investments for a few days. Given that Swaper only offers 14 and 30-day loans (at 12/14% interest rates) some cash drag unavoidable.

My interest rate on Swaper picked up again in January to 12.56% p.a. (= 113,88 EUR in January).

Given the recent shakeup in the P2P lending industry, I decided to do some further due diligence on all platforms that I am currently investing on. My findings gave me a comforting feel about Swaper. The platform was launched in 2016 and is owned by the Wandoo Finance Group, which has more than 100 employees in their offices in Riga, Madrid, Warszaw and Moscow.

The platform has not changed its business model and partners since 2016. According to Swaper (I reached out to them), the situation in terms of performance of all their loan originators has not changed and loans are still performing with the same level of quality as it was since Swaper started its operations.

What else? Swaper still runs its promotion that all investors signing up through this link will receive a “VIP Swaper Loyalty Bonus” if they invest more than 5000 EUR for three consecutive months! This means instead of a 12% profit, you’ll earn 14% if your account balance is above 5000 EUR for three consecutive months! 💸

Grupeer: Grupeer is doing great. My 15.000 EUR are fully invested and I received 167,22 EUR interest in January (= 12.32% interest p.a.). Absolutely no cash drag which is fantastic.

Grupeer is approaching the current ‘shakeup’ in the P2P market by directly engaging with its investors. Giving investors the opportunity to ask questions and by promising increased transparency moving forward. The co-founder and CEO released the below statement yesterday.

A released written statement on Grupeer’s website states that 40 employees work for Grupeer. The 2019 financial statements are planned to be published once filed with respective authorities. Further, Grupeer promises to show financial bloggers the development projects that are offered on Grupeer, as well as to introduce them to the loan originators and real estate developers in March and June.

Personally, I appreciate the messages and promised action, however, I am not planning to increase my investments on Grupeer until the promised actions have been implemented and financial reports have been shared.

What else? I updated my auto-invest portfolio to only include loan originators with A and B ratings (see full list of loan orginators and their ranking here. Have a look at my updated Grupeer review which shows my auto-invest settings.

Statement from Grupeer co-founder Alla Kisika

Twino: I am back to Twino. I had initially started investing on Twino in June 2015 and had a great experience, but then pulled out in February last year after Twino had published their 2017 financial report which showed a significant loss. In the meantime, Twino has released its 2018 financial report which shows a consolidated net profit of 9 mio EUR, marking the best financial result since Twino’s inception.

I decided to return to Twino with 5.000 EUR in late December. Similar to Swaper, Twino specializes in short-term loans (30-day loans) and provides payback guarantee. However, different from Swaper, most of the loans on Twino are paying only 10% interest p.a..

While interest rates on Twino are lower than on other platforms, I see Twino as a great platform to diversify my portfolio. It took a few weeks for me 5000 EUR to be fully invested, hence my January return was only 5,25 EUR in interest payments (= 1.26% interest p.a./This will certainly go up in February).

Twino has been operating since 2009 and currently employs more than 50 employees. Over the past 10 years, Twino claims to have issued consumer loans to the value of 1 billion EUR, funded by close to 20.000 investors.

What else? I will update my Twino Review over the coming weeks.

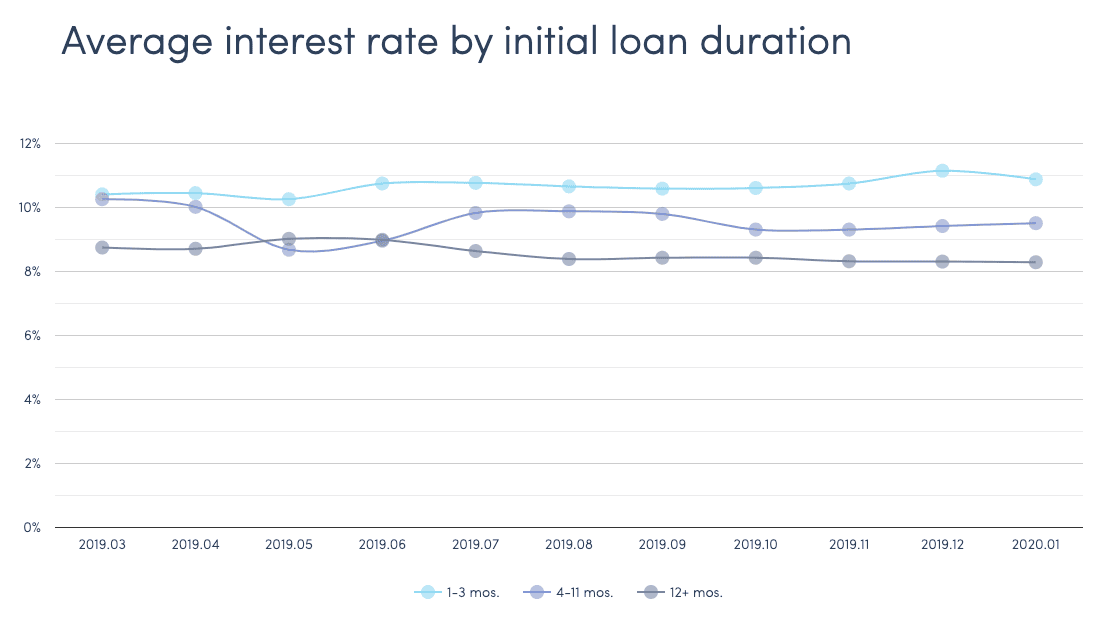

Twino average interest rates by loan duration (c) Twino

EstateGuru:EstateGuru maintains its excellent performance. After I increased my investments on EstateGuru to 5.000 EUR in late December, my auto-invest invested in 7 additional real estate projects (15 total now).

14 out of 15 projects are performing on time and 1 project is delayed by two weeks. The delayed project is secured with a first-rank mortgage (LTV 25.6%) and the borrower pays an additional 18.25% p.a. indemnity payment on the pending (delayed) interest payment, which is great for me.

As I mentioned in previous posts, most of my loans on EstateGuru are either bullet or full bullet loans, which means that either principals or both interest+principals are being paid in full at the end of the loan period. Unfortunately, that means that some months I receive large interest and principal payments, some months I receive nothing. In January, I received 24.79 EUR in interest payments, with an annual interest rate of 10.81%.

What else? My EstateGuru review explains details as well as shows how to receive a 0.5% bonus as a new investor. I just saw that EstateGuru has some new loans available (9.5% p.a. & 9.75% p.a.).

My EstateGuru portfolio as of 1 Feb 2020 (c) EstateGuru

CrowdEstate:My experience on CrowdEstate is negative and I am on my way out. 3 out of 8 projects are significantly delayed. Bankruptcy has been filed against one borrower (H.M Seafood OÜ) for non-payment of debts and the refinancing planned by the sponsor to repay another of my loans failed (Kreutzwaldi 59c, 65610 Võru (IX)).

I suspended my auto-invest in January and initiated my first withdrawal of 600 EUR two days ago. Overall I am not satisfied with the performance of the CrowdEstate platform, especially in comparison to EstateGuru, which is running like a charm.

After my withdrawal, I still have a total of 1,400 EUR invested in CrowdEstate.

Exchange–Traded Funds (ETF) Update – February 2020 🥳

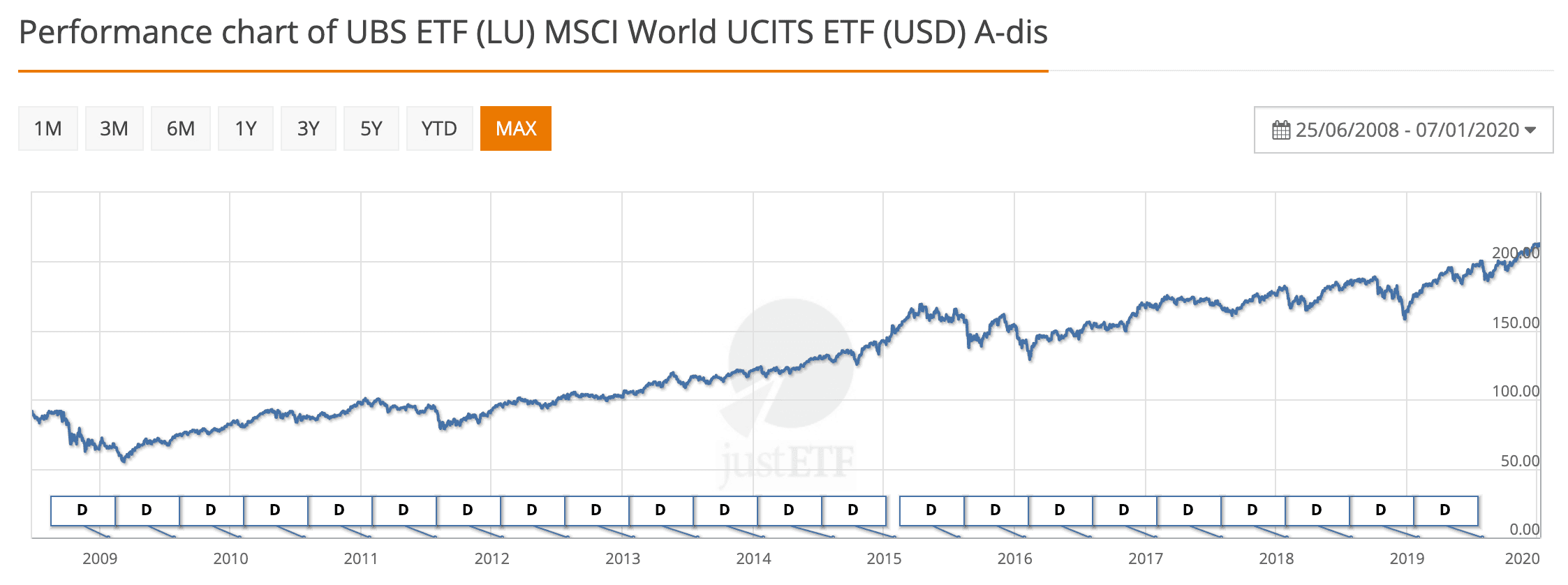

My decision to start investing in the MSCI World ETF back in 2016 was one of the best decisions of my life. I am explaining details in my ETF portfolio post, but in a nutshell, I believe there is no better and more cost-effective way to save & invest long term (e.g. for retirement) while earning passive income from dividends.

Since I started investing in the MSCI World ETF in 2016, the value has increased by 48.83%. The shares that I bought originally for 145.09 EUR apiece are today valued 212.18 EUR. Looking at the below graph of the MSCI World ETF (UBS UCTIS), I would say it’s hard to find a better, more stable, cost-efficient, and diversified investment. Why? More in my ETF portfolio post. 🥳

I committed to investing more in the MSCI World ETF to better balance my portfolio and desired investment ratio of 60%/40% (ETF/P2P). I am still waiting for a good moment to buy more ETFs at a lower price. More below.

Performance chart of MSCI World UCITS ETF (c) justetf.com

I had sold my DAX ETF in October 2019 (around 14,000 EUR) and I am still waiting for a good moment to invest it in the MSCI World. I am hoping that the MSCI World will drop temporarily in value (for example due to an economic shock) to allow me to buy the ETFs at a lower price.

As I mentioned in my January Blog Post, I decided to set up an ETF savings plan at 1000 EUR per month. I chose a free ETF savings plan which automatically buys MSCI World ETFs worth 1000 EUR on the first of every month. A savings plan allows to average the price of the ETF purchase. And thus reduces the risk of accidentally buying the ETF at a time when the market price is high. I explain more in this blog post.

Overall, my ETF portfolio continues to be a start. Over the course of January, my ETF portfolio has gained 0,26% in value in just one month. My total ETF investments are about 50,000 EUR which are valued 69,138.70 EUR today. In addition, I received about 3129 EUR in dividends over the past three years.

My ETF Portfolio since the beginning of this year (c) justetf.com

Overview of my current ETF portfolio (c) justetf.com

That’s it for my February 2020 Passive Income Update! If you are interested, please follow my journey on my Facebook page Financial Freedom Journey for more frequent updates. And as always: If you have any questions or comments, please pop them in the comment section below. Or get in touch via Facebook or Email.